Dutch nursery stock sector shows resilience, but differences between segments are growing

In the 2024-2025 season, the Dutch tnursery stock sector has once again demonstrated its ability to adapt to challenging circumstances. This is evident from the latest Tree Nursery Sector Report published by Van Oers. Although the sector as a whole remains stable, performance varies greatly between segments.

Unpredictable weather and high costs

The year was characterized by erratic weather conditions. The extremely wet and warm period of 2023-2024 did not materialize, but the climate remained unpredictable enough to hamper the planning and execution of cultivation and delivery activities. “The weather remains a factor that we cannot control, but which has a direct impact on our business operations,” according to the analysis in the report. Labor, energy, and raw material costs remained high, although raw material prices stabilized somewhat. Labor shortages remained a structural bottleneck, especially during peak periods.

Major differences between segments

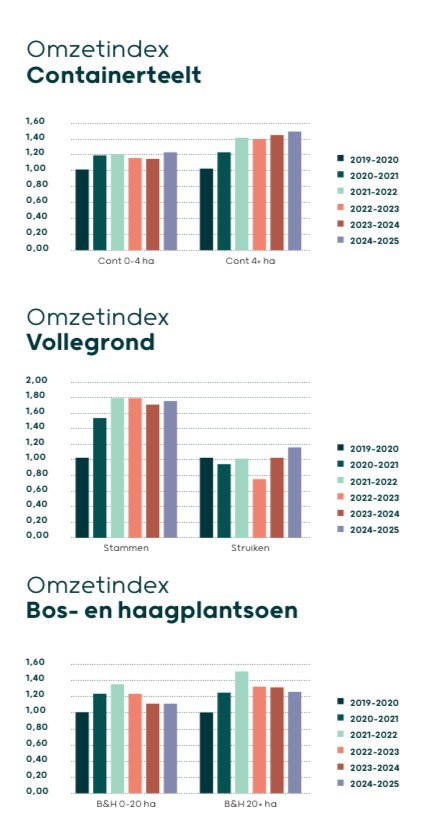

Turnover development varied greatly between the sub-sectors: Container cultivation companies achieved turnover growth of 5 to 10 percent, supported by stable demand. Forest and hedge plant companies saw their turnover fall by 5 to 10 percent. Tree and shrub companies recorded an even sharper decline. Trading companies lost an average of 7 percent of their turnover. According to Van Oers, the difference can mainly be explained by market pressure, shifting demand patterns, and the extent to which companies have their cultivation plans and cost structures in order. Slight shifts were visible in the export markets. New sales channels offered opportunities, but competition from abroad increased, putting pressure on prices. Segments with declining volumes felt this pressure particularly strongly.

Strategic choices are decisive

The report emphasizes that efficiency, cost control, and market-oriented working are more important than ever. Innovation in cultivation methods, sustainability, and the development of new sales markets are cited as keys to future-proofing. “Companies that invest now in flexibility and market expansion will have a head start,” says Van Oers.

Outlook

The tone for 2025 is moderately optimistic. Container cultivation companies seem to be able to maintain their growth trajectory, provided that demand remains stable. For forest and hedge plant companies and other segments experiencing a decline in turnover, the emphasis is on limiting price pressure and finding new markets.